Friday, December 01, 2006

Landbank logic vaults real estate shares

Parsvnath scrip zooms 75% on Day One; bulls outnumber bears for now

A little more than a decade ago, 42-year-old Pradeep Kumar Jain was a real estate broker for Delhi-based builders such as DLF, the Ansals and Unitech. On Thursday, when his real estate company Parsvnath Developers was listed on the National and Bombay Stock Exchanges, he ended up becoming a dollar billionaire.

Today, the self-made real estate baron, who’s been in the business for 23 years, saw his shares hit the stratosphere, rising 75% from its issue price of Rs 300 to close at Rs 526.30 a share. The company has on Day One crossed the $ 2 billion market-cap mark, with a valuation of Rs 9,715 crore.

With the promoters owning 80% of the newly-listed company, Jain and family are thus worth over Rs 7,800 crore.

Parsvnath’s listing marks a new high in the rapid unlocking of real estate values in grow-grow India. Between January, 2006, and November 30, real estate companies have added around Rs 54,000 crore of market-cap, two-thirds of it by Unitech alone. With Parsvnath

now getting listed, and Sobha Developers seeing a huge 108-fold oversubscription, and big daddy DLF waiting in the wings for a possible January issue, it is only a matter of time before the sector will top the Rs 200,000 crore market-cap mark.

Quite clearly, investors believe the real estate has nowhere to go but up. As Mark Twain said many eons ago: “Buy land, for they ain’t making any more of it no more.”

But not all are believers. “We are building towards a bubble”, says Jigar Shah, director of KR Choksey Shares and Securities. “When landbank valuations get reflected in share prices instead of cash flows and profitability of realty companies, share prices get inflated and then create a bubble,” warns Jigar.

In Parsvnath’s case, for example, the market is excited by the fact that the company acquired 108 million sq ft of land at an average cost of Rs 200 per sq ft whereas built-up property will be sold for an average of Rs 2,000-2,500 per sq ft. Even after construction and related costs, the margins will be nothing less than 100%.

Investors are jumping the gun, too. They have started discounting companies such as Century, Godrej Industries and Bombay Dyeing not for the businesses they are in, but the land they hold under their belt.

But if it’s primarily landbank logic that’s driving real estate valuations, there are two other reasons why bulls outnumber bears for now: limited supply of real estate scrip, and the sheer amount of money being raised for real estate investment. In January this year, the value of listed real estate companies was not even 1% of the BSE’s total market-cap. After the listing of Parsvnath, it’s closer to 2%, with the collective market-cap crossing Rs 73,000 crore.

Real estate buffs expect this to rise to 10% or thereabouts over the next four years as more real estate companies list themselves. And that’s merely what’s happening in India. Many realty companies are also listing subsidiaries abroad to raise funds for domestic investment.

Unitech, which is planning to raise $ 750 million, is the latest to seek a listing on the Alternative Investment Market (AIM), a subsidiary of the London Stock Exchange. Together with three other listings, the money raised is set to top $1 billion. And this does not include the billions raised by other global realty funds for investment in India and other emerging markets.

With that kind of money flowing into real estate, and given the kind of growth in infrastructure, hotels, retailing and special economic zones envisaged over the next decade, the bulls are carrying the day.

International hospitality majors such as Hilton and Accor are playing footsie with DLF and GMR. Bharti Wal-Mart, Kishore Biyani’s Future Group and Reliance are also wooing real estate developers with mind boggling lease rentals.

Jigar also admits that the strength and buoyancy of the Indian economy may act as a cushion and any bubble may be time to develop.

Uptrend may continue

The market will be eyeing the 14,000-mark in the coming week, betting on robust economic growth and strong results for December quarter from Indian companies. The domestic economy grew 9.2% in the July-September quarter from a year earlier, higher than market expectations of 8.90%.

Investors will continue to build fresh positions following a smooth rollover from November contracts to December series.

Expectations run high that FIIs may step up buying this month as allocations will be made for New Year calendar 2007. FII inflow in 2006 has reached $8.7 billion compared to a record inflow of $10.7 billion in 2005.

However, profit-booking can emerge at higher levels. The Sensex is already up 47.3% in calendar 2006 so far. A section of the market attributes the solid surge on the Indian bourses to increasing recognition of India’s long-term growth prospects. India’s growth drivers are a favourable demography (large share of young population), robust domestic consumption and acceleration in infrastructure creation.

Also the crawling crude oil prices, which are near $62 per barrel, may put brakes on the rally.

Dhampur Sugar Mills and Pioneer Embroideries will announce their results in the coming week.

Sensex advances 141 points

The market kept its rally intact as investors continued to mop-up shares at higher levels. The BSE Sensex advanced 141.45 points (1.03%) during the week ended 1 December, to 13,844.78, a record closing high. The S&P CNX Nifty rose 46.75 points (1.18%), to settle at 3,997.60, an all-time closing high.

Trading for the week began on a firm note. On Monday (27 November), the Sensex jumped 70.26 points, to 13,773.59, a record closing, partly on steady-to-firm Asian markets and partly due to short covering in the derivatives segment.

The Sensex plunged 171.64 points, to 13,601.95, tracking weak global markets on 28 November 2006. The BSE Sensex rose marginally by 14.78 points, to 13,616.73 on 29 November, amid a mixed trend in its constituents. On 30 November 2006, the Sensex finished with a gain of 79.58 points, at 13,696.31.

Sensex jumped 148.47 points to 13,844.78 on Friday (1 December), a record closing following a smooth rollover of November contracts and the sunsequent build up for December series, coupled with robust GDP figures.

Tata Power rose 1.32% to Rs 598.10. The company reported 61% growth in net profit for Q2 September 2006, to Rs 202.32 crore (Rs 125.67 crore). Total revenue rose 16.5% to Rs 1,279.17 crore, from Rs 1,097.21 crore.

Software major TCS rose 2.85% to Rs 1,183.30. TCS signed a 7-year deal worth $65 million for reorganising Somerfield's IT services. Somerfield is a leading UK-based, small-format food retailer.

Oil & refinery stocks slipped after the government announced a cut in retail prices of diesel and petrol by Re 1 and Rs 2, respectively, on Wednesday. Also crude oil prices moved near $62 per barrel, leading to a further fall in these stocks. Indian Oil Corporation (down 11.10% to Rs 445.50), Hindustan Petroleum Corporation (down 7.30% to Rs 289.75) and Bharat Petroleum Corporation (down 9.15% to Rs 342) declined.

Punj Lloyd jumped 15.46% to Rs 1,112. Punj Lloyd Group, a global infrastructure services provider, has bagged the order through Simon Carves, UK, a group company. The order is from PTT Polyethylene Company (PTT PE), a wholly-owned subsidiary of PTT Chemical Company, jointly with its partner Toyo Thai Corporation.

Ranbaxy Laboratories rose 0.10% to Rs 385.60. The company on Friday announced the acquisition of Be-Tabs Pharmaceuticals, the fifth largest generics company in South Africa, for $70 million.

Car major Maruti Udyog added 4.45% to Rs 952.60. In early-trade on Friday, the car major reported selling 55,033 vehicles in November, a 16.1% rise from a year earlier. The company said domestic sales rose an annual 20.7%, to 52,574, but exports fell 35.7% to 2,459 units.

Godfrey Phillips surged 42.49% to Rs 1,449.05, even as company denied rumours of a bonus issue and stock-split.

On 28 November 2006, Torrent Power (TPL), the umbrella company of the newly amalgamated generation, transmission and distribution businesses of the Torrent Group, settled at Rs 70.70 on BSE after listing at Rs 60 on BSE. Three companies, Torrent Power AEC (TPAL), Torrent Power SEC (TPSL) and Torrent Power Generation (TPGL), were merged into TPL giving shape to a scheme of arrangement.

GE Shipping re-listed on 27 November at Rs 264.65, and settled at Rs 222.70 that day, compared to the last trading price of Rs 336.70 of 7 November 2006. The scrip was relisted after giving effect to a restructuring scheme, whereby its offshore services division has been demerged into a separate company, and will be listed separately at a later date.

On 27 November, Lanco Infratech closed at Rs 241.40 on BSE, a marginal premium compared to the IPO price of Rs 240. Its public issue was oversubscribed nearly 12 times.

On 30 November, Parsvnath Developers settled at Rs 526.30, compared to the IPO price of Rs 300 per share. The company's paid-up equity capital is Rs 181.60 crore.

Mutual funds were net sellers for the first four days of the week, to Rs 262.48 crore, while FIIs purchased shares worth Rs 265.40 crore during the same period.

The domestic economy grew by 9.2% in the July-September quarter from a year earlier, higher than market expectations of 8.90%, data released earlier today showed. The annual growth rate in the second quarter of the 2006/07 financial year was higher than the April-June rate of 8.9%.

India's wholesale price index rose 5.45% in the 12 months to 18 November, higher than the previous week's annual rise of 5.29% due to a rise in mineral and manufactured product prices, data showed on Friday.

Movers & Shakers

- Maruti rallied sharply on reports of a 36% jump in the November sales numbers of its Omni and Versa models.

- Ranbaxy flared up on acquiring Be-Tabs Pharmaceuticals, the fifth largest generics company in South Africa, for $70 million.

- Punj Lloyd zoomed up on bagging a large contract for the construction of a LDPE plant in Thailand.

- Heritage Foods notched up significant gains on commissioning its first pilot retail store at Secunderabad.

- Banswara Syntex gained on bagging an export order worth Rs15 crore from Carreman Michel Thierry of France.

- Steel Strips Wheels shot up after showing a growth of 49% in its production and a growth of 35% in its sales in the month of November 2006.

Google Groups Issue

Google groups might be having some issues with reports sent today. You can STILL download older reports!

Come back and Download later if you get corrupted downloads or a blank page.

Update : Fixed now!

Weekly Close: Party continues.. !

Huge activity were seen during F&O expiry weak...Mid caps were also active.

Its clearly a party on the markets and there was activity in the mid caps as well. There was huge activity given that it was the FNO expiry. Markets were volatile after falling a big way on Tuesday on Global cues. But it was global cues which helped really. Japan had a booming economy against expectations that it was slipping. US economic data was mixed but the earlier GDP growth data was revised upwards and that had the US stocks rallying. The US housing prices and demand seems to be slipping. The worry also was the US Dollar which hit a 14 year low against the pound and was again created records in terms of weakness against the yen.

Leading the charge this week for the Sensex which closed up 1.12% was State bank. The Banking regulation act is to be presented and that had the interest flowing in. There was news of the petrol and Diesel price cut which fueled the Cement stocks and ACC and Ambuja were the Sensex gainers really. Maharashtra had more benefits with Sales tax being cut on diesel and also the surcharge being removed. We believe that reduction in taxes is positive but this cut in fuel prices is only robbing Peter to pay Pan with no real benefits. The Auto stocks fired up at the end of the week helped by strong sales numbers for November which were announced. Metal stocks were typically weak and also weak were the refinery stocks who will be really hit badly because of this fuel price cut. The software stocks were strong this week though they recovered from the initial lows not to end up gaining much. The dollar is weak and rupee was strong at Rs 44.5 against the dollar. However these software companies are resorting to innovative ways of increasing productivity. HCL T has increased the working hours. TCS has cut the number of holidays. Thats some way of beating the need for higher manpower in a crunch environment.

The leaders in the Nifty this week were, State Bank + 10%, ABB + 4%. ACC + 5%. Bajaj Auto + 4%. Gujarat Ambuja + 4%, Hero Honda + 7%, ITC +5%, Maruti + 4%, Rel com + 5%. Sun Pharma + 6%, Tata Power + 4%,

The losers this week were Bharat Petroleum -9%, HPCL -8%., Cipla -4%, Hindalco - 7%, Jet -4%. Sail -4%, Tisco -3%

India GDP galloping with agriculture a lagard; Honda Siel, Tyres, RSystems were some action stocks this week.!

The Indian economy grew by 9.2% in the July-September quarter (Q2) and 9.1% for the first half of the current fiscal. This is the highest such growth rate registered by the economy since the CSO started compiling quarterly GDP data 1996-97 onwards. The share of agriculture, forestry and fishing in the economy has come down to 17.2% in the first half, less than half the share of the primary sector in 1990-91, agriculture has grown by only a meagre 1.7%. Manufacturing registered a growth of 11.9% in the second quarter as against 8.1% in the corresponding period last year. The sector contributes to 16% of the GDP. The services sector, which now accounts for aboutt 66% of India's GDP, saw growth of 10.9% from a year earlier, accelerating from annual growth of 10.6% in the previous period. Within services, Trade, hotels and transport services expanded 13.9 percent, while financial services business grew 9.5 percent. Construction at 9.8% and financing, and real estate at 9.2 % and 9.5% were the drivers.

RBI statistics released upto 10th November indicate that credit growth is placed at 28.4% YoY. There has been a slowdown in % YoY terms largely on the back of a high base effect. Total deposit growth uptill the same period has increased to 20.7% YoY from 19.8% YoY on 27th Oct, 06. We seem to be headed towards a crunch period.

Mr Chidambaram said inflation was the only worrying factor in the overall macro-economic story and that we agree with. We believe that India's central bank will hike interest rates by at least 25 basis points in December or January. To add to the above.. Lower agriculture growth is a negative sign for the FMCG companies dependent on higher rural offtake.

We had a wow call on Honda Siel and that delivered wonders. The company is into engines gensets and pumpsets. The stock delivered a fantastic 15% gains and more expected in due course. The company has introduced LPG run products in the 1.5 KVA segment and that is a big positive. Going ahead they are trying to get the 5 KVA genset and that really will be the killer. We have a research note here do read

We had a Quickies call on R Systems which delivered a super 15% returns in a matter of days. The company is into offshore product development. It had fallen out of interest and with interest in offshore product development expected to increase the stock delivered. The stock remains inexpensive at around 14 times FY 08 even at current levels.

We had a research note on Apollo Tyres but the stocks we had calls on were Ceat and Premier Tyres. Both were fantastic super gains in a matter of days. Tyres benefit because of lower rubber prices and also because of lower costs of crude related raw materials. This sector has not performed and we caught it bang on. Do read the research note on Apollo tyres.

Mid caps have started performing and party may go on.. but be careful as always: Performance unbelievable this week too !

The mid caps have started joining the party and more is possible next week. However the worry is from the global markets where the US cues are not too encouraging. A weak dollar is certainly bad for the US markets we believe. However the US GDP growth has been the saviour and hopefully these negatives should pass. However, as investors its best to play safe. Get some cash off the table. Put stoplosses and all fresh entries should be with stoplosses.

FII: FII's net buyers of ..

FII Gross purchases Rs 4073 Cr Gross Sellers Rs 3815 Cr Net Buyers Rs 258 Cr

MF Gross Purchases Rs 589 Cr Gross Sellers Rs 677 Cr Net Sellers Rs 88 Cr

This buying by FIIs is certainly a positive. Flows are back.. However better to ignore this data which is for the last day of the expiry. This in conjunction with FII FNO data would be more useful.

Riding the retail wave

With India's burgeoning middle-class, and a relatively young population - about 500 million Indians are below the age of 24 - there is growing hunger for credit cards, auto and consumer loans, and a host of other products.

And banks, especially the new crop of private sector institutions, have been feeding this monstrous demand for credit with a slew of innovative products. India's retail banking industry grew by a whopping 120 per cent in 2005, and total asset size has topped US$ 65 billion.

Download here

Sensex gains 148 points

Driven by the sharp gains in heavyweight, auto, capital goods, FMCG and banking stocks the market ended on a buoyant note for the third consecutive session. After registering gains of 80 points yesterday, the Sensex resumed with a positive gap of 34 points at 13730. Maintaining its upward bias, extensive buying in several sectoral stocks saw the index edge past the 13850 mark and touch an all-time high of 13858, up 162 points for the day. The Sensex closed the session with gains of 148 points at 13845. The Nifty touched an all-time high of 4001 and closed the session at 3998, up 43 points.

The breadth of the market was positive. Of the 2,650 stocks traded on the BSE, 1,516 stocks advanced, 1,063 stocks declined and 71 stocks ended unchanged. Among the sectoral indices, the BSE Auto index gained 2.84%. The BSE CG index added 1.84%, the BSE FMCG index advanced 1.61% and the BSE Bankex was up 1.53%. The remaining indices were up around 1% each.

Among the Sensex stocks Tata Motors vaulted 4.14% at Rs843, Bajaj Auto soared 3.91% at Rs2,748, Hero Honda surged 3.91% at Rs772, SBI advanced 3.52% at Rs1,360, Reliance Communication gained 3.03% at Rs442, Ranbaxy spurted 2.94% at Rs383, Dr Reddy's soared 2.62% at Rs770 and Reliance Energy was up 2.33% at Rs540.

Among the auto and auto ancillary stocks Balkrishna Industries surged 4.74% at Rs581, Punjab Tractors soared 4.58% at Rs250, Escorts advanced 3.62% at Rs122 and Amtek Auto added 3.58% at Rs367. Maruti Udyog, Cummins India and Mahindra & Mahindra gained above 2% each. However, Apollo Tyres, Asahi India and Exide Industries closed in negative territory.

BPL at Rs71.45, Godfrey at Rs1,449.05, Lakshmi Machine Works at Rs34,051.65, Thomas Cook at Rs546 and Flex Industries at Rs82.65 hit the upper circuit breaker. On the other hand Torrent Gujarat Biotech at Rs10.12 and Tips Industries at Rs27.80 hit the lower circuit on the BSE.

Over 41.96 lakh Parsvnath Developers shares were traded on the BSE followed by Dena Bank (25.75 lakh shares), Reliance Communication (16.99 lakh shares), Lanco Infratech (15.99 lakh shares) and Alstom Project (15.33 lakh shares).

Sensex about 150 points short of 14,000

The market’s gravity defying rally continues. The Sensex today struck an all-time high, and made a move closer to 14,000. A smooth rollover from November contracts on Thursday to December series coupled with robust GDP growth data released during trading hours on Thursday, lifted the Sensex by almost 150 points today. Auto scrips, PSU banks and index heavyweight Reliance Industries were at the forefront of today’s rally.

The Sensex jumped 148.47 points (1%), to settle at 13,844.78, a record closing. It is now just about 150 points away from the psychologically important 14,000 milestone.

S&P CNX Nifty advanced 43.10 points (1%), to settle at 3,997.60, a record closing. It also hit 4,001.30, a life high for the index.

The BSE clocked a turnover of Rs 4,451 crore, compared to Thursday’s Rs 4,854 crore.

The market-breadth was strong. For 1,484 shares that rose on BSE, 1,080 declined. As many as 72 stocks were unchanged.

The salient feature of the recent rally has been a surge in small-cap and mid-cap shares. Even as the Sensex kept striking a string of record highs over the past few days, small-cap and mid-cap stocks had lacked momentum.

From 6,531.39 on 28 November, the BSE Small Cap Index has risen 187.35 points (2.8%) in the past three trading sessions to current 6,718.74. From 5,651.21 on 28 November, the BSE Mid Cap Index has gained 124.21 points (2.1%) in three days, to current 5,775.42. The Sensex added 242.83 points (1.7%) in this three-day period, from 13,601.95 on 28 November 2006.

The market sentiment remains bullish due to strong FII-inflows and an upward revision in earnings growth by brokerages, on the back of strong Q2 results. Widespread optimism that FIIs may step up buying this month, as allocations are made for calendar 2007. FII inflow in 2006 has reached $8.7 billion, compared to a record inflow of $10.7 billion in 2005.

The BSE Sensex is up 47.3% in calendar 2006 so far. From 4,644 on 23 June 2004, it has galloped 198% in less than two-and-a-half years. A section of the market attributes the solid surge on the Indian bourses, to increasing recognition of India’s long-term growth prospects. India’s growth drivers are a favourable demography (large share of young population), robust domestic consumption and acceleration in infrastructure creation.

In today’s trade, Ranbaxy Laboratories surged nearly 4% to Rs 385.60, with the stock rallying in late-trading after the company announced the acquisition of Be-Tabs Pharmaceuticals, the fifth largest generic drugs company in South Africa, for $70 million.

Auto shares dominated the proceedings on decent-to-strong sales numbers for November. Bajaj Auto rose 4% to Rs 2,751, after its total sales rose 33% in November 2006, to 2,43,713 units from a year ago. Bike sales rose 36% to 2,14,321 units and sales of three-wheelers were up 71% at 29,384 units. Exports rose 56% to 36,086.

Hero Honda rose nearly 2% to Rs 757.35. Hero Honda today launched two variants of its CD series motorcycles, CD Deluxe and CD Dawn, in the 100-cc, entry-level segment.

Tata Motors surged 4% to Rs 844.25, on expectations of strong sales for November 2006. Tata Motors is likely to disclose its monthly sales figures today.

Car major Maruti Udyog added nearly 3% to Rs 952.60. In early-trade today, the car major reported selling 55,033 vehicles in November, a 16.1% rise from a year earlier. The company said domestic sales rose an annual 20.7%, to 52,574, but exports fell 35.7% to 2,459 units.

PSU banks were in demand after the latest data showed lower-than- expected rise in inflation. SBI jumped 4% to Rs 1,369.90. The stock hit Rs 1,370, a life high for the scrip.

Cellular services provider Reliance Communications rose 3.7% to Rs 445.25. The scrip struck Rs 446.90, an all-time high. A staggering 16.8 lakh shares changed hands in the counter on BSE.

Reliance Energy gained 2.2% to Rs 540.05. As per reports, Maharashtra Electricity Regulation Commission has directed the company to discontinue levy of load management charges.

Reliance Industries gained 1.3% to Rs 1,262.25. A strong 7.4 lakh shares changed hands in the counter.

A host of power equipment makers/solutions provider to the power sector surged. Alstom Projects jumped 9.7% to Rs 468.90, Bharat Bijlee gained 7.9% to Rs 1,205, ABB surged 7% to Rs 3,747, Voltamp Transformers gained 5.8% to Rs 631.80, Areva T&D rose 5% to Rs 972.10, Siemens advanced 4.7% to Rs 1,182, and KEC International gained 3% to Rs 390.

Construction firm Punj Lloyd jumped 7.6% to Rs 1,112, after the firm said it had an order worth Rs 1,000 crore to construct an LDPE manufacturing plant in Thailand.

Gas cylinder maker Everest Kanto Cylinder jumped 10% to Rs 606.50, on expectation that the firm will announce a large order in the next few days.

Thomas Cook India jumped 10% to Rs 564.05, ahead of the company's board meeting to consider merger and acquisition proposals.

Sponge iron and steelmaker Raipur Alloys and Steel jumped 14% to Rs 140 after the company informed Friday that Reliance Long Term Equity scheme of Reliance mutual fund purchased 9.62% in it. The fund acquired about 1.26 million shares on 29 Nov, the company said.

Essar Shipping jumped 17.8% to Rs 27.80. The company today said it had received a letter from promoters, Essar Shipping & Logistics, to delist the company's shares from BSE. The company has called a board meeting on Saturday, to consider delisting.

McLeod Russel India rose 2.6% to Rs 109.95 on reports that the company had acquired 72 % stake in Moran Tea Co for Rs 41.50 crore. The acquisition of Moran Tea will add Rs 32 - Rs 33 core to McLeod's annual revenue, Managing Director Aditya Khaitan said.

Paramount Communications jumped 8.5% to Rs 255. The scrip rose on heavy volume of 37.1 lakh shares on BSE. A block deal of 2,67,268 shares was executed in the stock on BSE, at Rs 247.

Global Vectra Helicorp jumped 20% to Rs 192, on reports that the government is planning to raise FDI limit to 74% in helicopter services, non-scheduled airline operations and regional airlines using small aircraft. The current ceiling for airline services is 49%.

Shoppers’ Stop rose 3% to Rs 702.25, after the company formed a 50:50 joint venture with Swiss firm Nuance Group, a global market leader in the airport retail space, to operate duty free shops at international airports in India.

Ispat Industries was flat at Rs 11.09. The company has reduced prices of hot-rolled coils by Rs 400 - Rs 600 per tonne, with immediate effect.

Tamil Nadu Newsprint & Papers gained 1.5% to Rs 94. The company said on Friday that Reliance Growth Fund and Reliance Portfolio Management Services, have picked up an additional 0.32% stake in the company. This takes their collective stake to 5.08%

Nandan Exim dropped 5% to Rs 10.55 in volatile trade. Initially, the scrip had surged 5% to Rs 11.65 after a block deal of 5 lakh shares was executed in the scrip on BSE, at Rs 11.45.

Steel Strips Wheels rose 3% to Rs 155.90, after the company said on Friday its November sales of wheel rims rose to 4,10,086 units, up 35% from a year ago. It produced 4,00,824 wheel rims in November compared to 2,68,555 rims same month a year ago.

Flex Industries (up 20% to Rs 82.65) surged for the second day in a row after the company said on Thursday that the merger of two other group companies, had been cleared by the Delhi High Court. Group companies, Flex Engineering and FCL Technologies, will be merged with Flex Industries, enabling accumulation of resources under a single entity that will provide end-to-end packaging solutions.

Financial Technologies shed 1.8% to Rs 2,062. The company on Thursday said it had in principle approval from the Financial Services Commission, Mauritius, for setting up an international multi-commodity exchange styled Global Board of Trade.

TRF lost 0.8% to Rs 425. ACC has cut its stake in the company by 2%, bringing it down to 4.54%, informed TRF.

HCL Infosystems rose 0.3% to Rs 165. The personal computers market recorded 24% growth in the third quarter ended 30 September 2006. HCL Infosystems has retailed its number two slot with a market share of 12%.

Graphite India rose 1.4% to Rs 303, after the company fixed 18 December 2006 as a record date for 5-for-1 stock-split.

India's economic growth accelerates

India's economic growth accelerated to 9.2 percent in the July-September quarter compared with a year ago, the government said Thursday, bringing it closer to China's sizzling growth rate.

Fueled by a brisk expansion of the services sector and a surge in manufacturing output, India's gross domestic product expanded at a faster pace than the 8.9 percent growth in the previous quarter.

The numbers beat expectations and prompted many analysts to revise their forecasts for the full fiscal year through March 2007.

"We are revising our full year growth estimate to 8.4 percent from 7.9 percent," said Shubhada Rao, chief economist at Yes Bank.

If that projection comes true, it would be the fourth straight year of 8 percent-plus growth for India, one of the world's fastest-growing economies after China, which grew 10.4 percent in the July-September quarter.

Some analysts expected GDP growth to moderate through the later part of the year because of high oil prices and a possible slowdown in global demand for Indian exports.

But manufactured output rose 11.9 percent during the July-September period compared with 8.1 percent in the same period last year. The growth was mostly driven by a surge in exports.

High oil prices have also pushed inflation and interest rates, and many thought that would also impact services such as transportation, banking and trade.

But the services sector, which accounts for more than half of India's GDP, continued to be buoyant. Trade, hotels and transport services expanded 13.9 percent, while financial services business grew 9.5 percent.

"The upside surprise relative to our forecast came almost entirely from the unexpected acceleration in service sector activity," said Rajeev Malik, a Singapore-based economist with JP Morgan Chase Bank.

JP Morgan was revising its forecast for India's economic growth in the current fiscal year to 8.4 percent from an earlier projection of 8 percent, he said.

Malik said he expects India's central bank to hike key interest rates by at least a quarter percentage point in December or January to keep inflation under check. "The Indian economy is not overheating, though the impressive growth momentum is showing some signs of excesses."

The sluggish performance of the agriculture sector, however, remained a concern. During the July-September period, farm output grew just 1.7 percent, sharply down from 4.1 percent in the same quarter a year ago.

About two-thirds of India's 1 billion people live on agriculture and most of them earn less than a dollar a day. They has been left untouched by India's economic boom over the past decade -- which has been driven by the expansion of industry and services.

IPO hunters lose Rs 14k cr in one year

Primary market investors have hit the jackpot with many of the past new issues attracting hefty premium on listing and recording sharp appreciation in the subsequent weeks. But, not all primary market investors have been lucky enough to gain from the boom as some of newly listed companies have lost momentum after the initial euphoria.

Investors have lost wealth to the tune of Rs 14,000 crore in about 60 companies listed in the past one year as their share prices have fallen substantially since listing. Some of them have even slipped below offer prices, going by the trend on the BSE.

Reliance Petroleum (RPL) topped the list, recording a m-cap loss of Rs 8,307 crore since its listing on May 11, ’06. From its listing price of Rs 85.5, the RPL stock price has fallen 22% to end at Rs 67 on Wednesday. The Sensex rose 9.5% during the period. The scrip, however, is still quoting at a premium to the offer price of Rs 60 per share.

Apart from RPL, there are many other companies whose stocks have lost ground but still quoting above offer prices. GTL Infrastructure, Tantia Construction, Inox Leisure, ABG Shipyard, Plethico Pharmaceuticals, Royal Orchid and PVR are few notable examples of this phenomenon. They are currently quoting at a discount of 3% to 32% (Tantia Construction) to listed prices but at premium between 12% and 301% (GTL Infrastructure) to offer price.

Analysts cite many reasons for these companies’ underperformance against the market which has been on a dream run after crashing below 9,000 in June. Large companies like RPL is a long term bet given the nature of the project the company has been implementing, said an analyst at a leading domestic brokerage.

In April this year, RPL had gone public with an offer of 135 crore shares through the 100% book building route. The issue proceeds are being utilised to part finance the Rs 27,000-crore export-oriented refinery being set up in a special economic zone at Jamnagar in Gujarat. The project is likely to go on stream by December ’08.

Analysts also said new listings could not sustain momentum probably because the market felt offer prices were higher than expectations. This could be one reason why some of the IPOs are quoting below offer prices in the current market. As many as 30 of the 60 new listings are currently trading below their respective offer prices.

GVK Power, Pyramid Retail, Prime Focus, Repro India and Global Vectra are few such examples.

Nifty hits 4,000 in late-trading

The S&P CNX Nifty pierced the 4,000 mark at the fag end of trading. The BSE Sensex surged over 150 points due to buying in auto scrips, PSU banks and index heavyweight Reliance Industries.

A smooth rollover from November contracts on Thursday to December series coupled with robust GDP growth data released during trading hours on Thursday, provided support on a day when Asian markets traded mixed.

The Sensex’s provisional closing was 13,853.81, a gain of 157.50 points. The barometer index struck a new record of 13,857.81 at 15:01 IST.

The Nifty had gained 43.20 points (1%), to 3,997.70, as per the provisional closing. It also climbed to a record high of 4,001.30.

The BSE clocked a turnover of Rs 4,451 crore.

Ranbaxy Laboratories surged nearly 4% to Rs 385.60, with the stock rallying in late trading after the company announced the acquisition of Be-Tabs Pharmaceuticals, the fifth largest generics company in South Africa, for $70 million.

Auto shares dominated the proceedings on decent-to-strong sales numbers for November. Bajaj Auto rose 4% to Rs 2,751 after its total sales rose 33% in November 2006, to 2,43,713 units from a year ago. Bike sales rose 36% to 2,14,321 units and sales of three-wheelers were up 71% at 29,384 units. Exports rose 56% to 36,086.

Hero Honda rose nearly 2% to Rs 757.35. Hero Honda today launched two variants of its CD series motorcycles, CD Deluxe and CD Dawn, in the 100-cc, entry-level segment.

Tata Motors surged 4% to Rs 844.25, on expectations of strong sales for November 2006. Tata Motors is likely to disclose its monthly sales figures today.

Car major Maruti Udyog added nearly 3% to Rs 952.60. In early-trade today, the car major reported selling 55,033 vehicles in November, a 16.1% rise from a year earlier. The company said domestic sales rose an annual 20.7%, to 52,574, but exports fell 35.7% to 2,459 units.

PSU banks were in demand after the latest data showed lower-than- expected rise in inflation. SBI was jumped 4% to Rs 1,369.90. The stock hit Rs 1,370, which is a life high for the scrip.

Cellular services provider Reliance Communications rose 3.7% to Rs 445.25. The scrip struck Rs 446.90, an all-time high. A staggering 16.8 lakh shares changed hands in the counter on BSE.

Reliance Energy gained 2.2% to Rs 540.05. As per reports, Maharashtra Electricity Regulation Commission has directed the company to discontinue levy of load management charges.

Reliance Industries gained 1.3% to Rs 1,262.25. A strong 7.4 lakh shares changed hands in the counter.

India's growth story just got better

GDP grows 9.2% in Q2, fastest half-year rise since 1991.

India’s economic growth rate accelerated to 9.2 per cent in the July-September quarter from 8.4 per cent in the year-ago quarter on the back of a strong performance by the manufacturing and services sectors, raising the likelihood of interest rates being raised in January 2007.

Taken along with 8.9 per cent growth in the first quarter of the current financial year, this comes to 9.1 per cent growth for the first six months of 2006-07. Finance Minister P Chidambaram said this was the highest first-half GDP growth since 1991-92, when economic reforms were initiated.

He added that the 9.2 per cent growth clocked in the second quarter was among the highest growth rates in recent years.

“Higher growth rates were only seen in the fourth quarter of 2005-06, which saw 9.3 per cent growth and in the third quarter of 2003-04, which saw 11.3 per cent rise. This, however, was on a low base of 1.5 per cent,” he said.

After today’s numbers, economists said they might look at revising their growth forecast for the whole year. “Overall, we are revising up our full-year forecast marginally to about 8.2-8.3 per cent from 8.0 per cent,” JP Morgan Economist Rajiv Malik told agency.

“With GDP growth for the first half at 9.1 per cent, it is certain that there will be an upward revision for the full year. If the growth momentum is maintained, I see full-year GDP growing at close to 9 per cent,” added CRISIL Chief Economist Subir Gokarn.

Asked to comment on the expected annual rate of growth, Chidambaram said, “There is no limit to my expectation on GDP growth.”

He also played down concerns of increased pressure on interest rates on account of the high economic growth rate.

“There is ample liquidity in the system. Only yesterday, the Reserve Bank of India absorbed Rs 2,400 crore through reverse repo.” He endorsed the RBI’s view that it was premature to think of the economy “overheating.”

The finance minister said all sectors had done better in the second quarter than in the first one, barring agriculture and mining and quarrying. Commenting on the 1.7 per cent growth in agriculture, he said this was not unusual.

“The second quarter is always a lean quarter, as only a part of the kharif crop has come in, and the rabi crops come in in the third and the fourth quarters,” he felt.

“One of the worrying factors is the slightly high inflation, which is largely driven by supply side constraints. But with better supply side management and sugar and wheat stocks building up, I am confident that inflation can be tamed,” the minister said.

Poweryourtrade.com Trading Calls

Buy Bharti Airtel with stop loss of Rs 610 for target of Rs 696

Buy HDFC Bank with stop loss of Rs 1060 for target of Rs 1230

Buy Bharti Airtel below Rs 634 with stop loss of Rs 626; This is a day trading recommendation

Short sell IPCL above Rs 273 with stop loss of Rs 278; This is a day trading recommendation

Buy Biocon with stop loss below Rs 367 for target of Rs 383–387

Sell BPCL with a stop loss above Rs 350.10 for target of Rs 336

Poweryourtrade.com Trading Calls

Buy Rain Calcining at around Rs 48.85 with stop losso of Rs 48. (Intra-day call)

Buy Vakrangee Software at around Rs 251.35 with stop loss of Rs 247. (Intra-day call)

Sharekhan Commodities Buzz dated December 01, 2006

Bullions: Win-win situation

Gold prices rose to the highest level in more than three months following a drop in the value of the greenback against the euro and the sterling. A strong sterling rose up to a 14-year high level of $1.9694 on the back a stronger economy. Further expectations that the Bank of England may raise rates put pressure on the dollar on the narrowing yield spread.

Download here

Market may witness profit-taking in early trades

The market is likely to remain subdued during the intraday trades. The weak FII participation in the last couple of sessions is also weighing on the sentiment. While, the domestic market the Nifty may witness resistance at 3975 on the upside while the near-term support at 3945 and below this the next support at 3925 on the downside. The Sensex has a likely support at 13650 and could witness resistance at 13800.

US indices ended with marginal loss on thursday, with the Dow Jones declined 5 points to close at 12,222 while the Nasdaq slipping by nearly half a points at 2432.

Indian ADRs had a mixed outing on the US bourses. Infosys, Wipro, Dr Reddy's, ICICI Bank, HDFC Bank, MTNL, Rediff closed positive and Satyam, Tata Motors, VSNL and Patni Computers declined 1% each.

In the commodity segment, the Comex gold for the February adavnced $11.10 to settle at $652.90 an ounce. The Nymex light crude oil for January delivery jumped 67 cents to close at $63.13 a barrel, while the London brent crude was up 62 cents at $59.46 per barrel.

Northgate Technologies Ltd.

Northgate is the best play amongst the listed stocks on the global Internet revolution. The Company is expected to get a major fillip from rapidly growing online advertising industry and rising popularity of e-commerce. Both the offerings of the company, Axill (online advertising network/exchange) and Globe7 (patented SIP based VoIP phone), are fast gaining popularity and mileage worldwide especially in US. Company’s revenues and earnings grew 58.7% and 199% respectively in FY06. It has already surpassed FY06 numbers in H1 FY07. At a P/E valuation of 27.7x based on annualized H1 FY07 EPS of Rs30, it is the most inexpensive play on the Internet revolution when compared with significantly higher valuations of Info Edge and global counterparts like Google, Rediff, etc. We expect significant upside from the current levels

5 Intra-day Stock Ideas

NIFTY (3955) SUP 3941 RES 3967

BUY Hero Honda (742) SL 736 T 751, 755

BUY GAIL (267) SL 262 T 275, 277

BUY Bharti Airtel (631) SL 625 T 641, 643

SELL Tata Tea (718) SL 725 T 709, 706

SELL HPCL (282) SL 287 T 275, 271

Indiainfoline - Strategy Inputs for the Day

Overheated…cool down a little!

Winter is on my head, but eternal spring is in my heart. – Victor Hugo

Winter has been on the bear’s head ever since summer May. And the bulls have had a favorable weather since then. The F&O settlement day is behind us now. It is the start of a new derivative series. The overall rollover was in line with expectations, but the same in Nifty Futures was lower than the market-wide rollover. Also, there are indications that investors and traders alike are getting a bit jittery about holding long positions. More short positions have been carried forward this time around, leading to a fall in the cost-of-carry and in the Nifty Futures premium to the spot Nifty. Market observers, including us, have been repeatedly warning of overheated conditions in the market and a possible correction. Though the same has not materialised so far, it may happen without any prior warning. FII inflows have also slowed down in the past few days, and if the trend continues the bulls will find it tough to retain their hold on the proceedings. Having said that the scene is not all that grim either, as the long-term outlook for the Indian economy and corporate earnings remains upbeat. Just that the market has rallied quite a bit since the carnage in May and June without any significant break and needs to pause. Globally, markets in the US ended flat overnight while Asian indices are mixed. Crude is still well above the $62 per barrel mark. We are expecting a cautious opening and a lackluster day ahead of the weekend.

Hero Honda could be the focus of attention as it has reported a 12% year-on-year increase in November sales. But, compared to the previous month, which was a festival month, the company's sales are down 22.6%. Moreover, a national daily reports that the Hero Group is considering entering the car manufacturing and auto component space. The company is also making an announcement this afternoon in Mumbai. Indiabulls is likely to gain as steel baron Lakshmi Mittal and Farallon Capital have together picked up 13.3% stake in its real estate arm for almost Rs4.5bn. Another stock to keep an eye on is Thomas Cook amid reports that it is buying Travel Corporation of India. City Union Bank is likely to be in action as a L&T arm has picked up a 10% stake in the Kumbakonam-based bank. However, the deal could face some hurdles as the RBI doesn't allow any corporate house to have more than 5% stake in a bank.

US shares closed nearly unchanged on Thursday. The Dow Jones was down 4.80 at 12,221.93, while the broader S&P 500 closed nearly flat at 1,400.63. The Nasdaq too finished nearly unchanged at 2,431.77.

Crude oil for January delivery gained 67 cents to settle at $63.13 a barrel on the New York Mercantile Exchange, rising after Wednesday's weekly oil inventories report showed a surprise dip in crude, gas and distillate supplies. The contract was quoting 29 cents lower at $62.84 in extended trading in Asia.

COMEX gold for February delivery jumped $11.10 to $652.90 an ounce. Treasury bond prices rallied, lowering the yield on the 10-year note to 4.46% from 4.52% late on Wednesday. In currency trading, the dollar continued its retreat versus other major currencies.

Among the Indian ADRs, Patni was down nearly 1%, Wipro gained 2.35% and Dr. Reddy's rose 1.6%.

European shares closed lower after weak US manufacturing data put further pressure on the dollar. However, gains in shares of Rio Tinto and BHP Billiton helped curb losses. The French CAC-40 finished down 1% at 5,327.64, the German DAX Xetra 30 lost 0.9% to 6,309.19 and the UK's FTSE 100 declined 0.6% to 6,048.80.

In the emerging markets, ended lower by 0.1% at 41,931, while the IPC index in Mexico rose 0.75% to 24,962 and the RTS index in Russia gained 0.65% to 1776.

Asian stocks were mixed this morning. The Nikkei in Tokyo advanced 45 points to 16,320 while the Hang Seng in Hong Kong was down 56 points to 18,904. The Kospi in Seoul was flat at 1433 and the Straits Times in Singapore added 4 points to 2842.

The Morgan Stanley Capital International Asia-Pacific Index rose 0.2% to 136.62 as of 11:30 a.m. in Tokyo. The measure is set for a 3.1% jump this week, the most since the five days to Aug. 18.

Indexes advanced in Taiwan, Indonesia and China and fell elsewhere. Markets were closed in the Philippines.

Major Bulk Deals:

Morgan Stanley has sold Gitanjali Gems; Prudential ICICI MF has bought Gujarat Apollo Equipment; UTI MF has sold IDFC; Morgan Stanley has bought IOL Broadband but Bear Stearns has sold it; Lehman Brothers has purchased Pioneer Embroidery and T. Rowe Price has sold SREI Infrastructure.

Insider Trades:

TVS Motor Company Limited: T K Balaji, Director has sold in open market 29250 equity shares of TVS Motor Company Limited on 22nd November, 2006.

Goldiam International Limited: Mr. Rashesh M Bhansali (Vc Chairman & Mg. Director) has purchased from open market 57437 equity shares of Goldiam International Limited on 27th November 2006.

Nava Bharat Ventures Limited: P. Punnaiah, Director has sold in open market 7946 equity shares of Nava Bharat Ventures Limited on 27th November, 2006.

Market Volumes:

The turnover on NSE was up by 57% to Rs127.25bn. BSE Technology index was the major gainer and gained 1.37% and BSE Bank index (up 1.29%) was the other major gainer. However, BSE Metal index lost 1.13%, BSE Consumer Durable index (down 0.63%) and BSE Auto index (down 0.29%) were the other major losers.

Volume Toppers:

Parsvnath Dev, Torrent Power, Hindalco, R Com, ACE, IVRCL Infra, SAIL, NTPC, Zee, Guj NRE Coke, ITC, Indiabulls, ONGC, Gitanjali Gems, Ranbaxy and GE Ship.

Delivery Delight:

Aditya Birla Nuvo, Aurobindo Pharma, Bank of India, BHEL, Bharti Airtel, Dr Reddys, Educomp, GAIL, HDFC Bank, ICICI Bank, Indiabulls, Infosys, ITC, IVRCL Infrastructures, M&M, McDowell & Co, NIIT LTD, Rain Calcining, Reliance Communications, Sun TV, Wipro and Zee Telefilms.

Brokers Recommendations:

Elecon Engineering – Buy from Prabhudas Liladhar

Dr Reddy’s Labs – Neutral at HSBC

Long Term Investment:

BHEL

Major News Headlines:

MTNL revises Q2 net profit to Rs1.1bn from Rs1.2bn

IOC, other refiners cut Jet Fuel prices by 2.5%

PSL secures orders worth Rs3.08bn

Reliance units hire ICICI Bank for $925mn loan

GMR Infrastructure unit in pact with ACCOR for Hyderabad hotel

BHEL to expand annual capacity to 10,000 MW pa

How Market Fared

Future in favour of bulls

The Bulls ended with healthy gains, banking on impressive economy data and short covering in late afternoon trades. Fresh buying in Banking and Technology stocks towards the fag end also boosted the indices. Firm global markets once again aided the domestic bourses to surge at open but however bulls couldn’t hang on to their gains as Bomb scares in parliament and selling pressure weakened the key indices. The bulls, however against all odds gained momentum led by gains in HDFC Bank, BHEL, Bharti Airtel and Infosys. Finally, the BSE Benchmark Sensex gained 79 points, to close at 13696. NSE Nifty was up 26 points to close at 3954.

L&T slipped 1.2% to Rs1364. The company’s JV secured Rs4.56bn order from NTPC. The scrip touched an intra-day high of Rs1398 and a low of Rs1359 and recorded volumes of over 6,00,000 shares on NSE.

Parsvnath Developers one of the leading real estate developers in the country made an impressive opening on the bourses. The stock opened at Rs540 as against the issue price of Rs300, at premium of 80%. However the scrip ended at Rs526 (up 75%).It touched an intra-day high of Rs575 and a low of Rs456 and recorded volumes of over 4,00, 00,000 shares on NSE.

Reliance Communication gained 1.3% to Rs427 as reports stated that the company was setting its sights on distribution of mobile content to service provider across the globe. The scrip touched an intra-day high of Rs432 and a low of Rs421 and recorded volumes of over 79,00,000 shares on NSE.

PSL surged 1.8% to Rs205 after the company secured Rs3.08bn order to supply Carbon Steel Barc Line Pipes to BINA Refinery in Sultanate of Oman. The scrip touched an intra-day high of Rs213 and a low of Rs201 and recorded volumes of over 1,00,000 shares on NSE.

Banking stocks witness fresh buying in choppy trades. Index heavy weights like led from front. HDFC Bank, ICICI Bank and SBI were among the major gains. However Mid-Cap stocks witnessed profit booking Bank of Baroda fell by over 1.8% to Rs260, Syndicate Bank was down 0.9% to Rs81and OBC lost 0.55 to Rs245.

Technology stocks ended with smart gains. IT front runner Infosys after slipping yesterday gained 1% to Rs2179, Satyam Computer gained 1.8% to Rs459 and Wipro advanced 2.9% to Rs599. Among the Mid-Cap stocks NIIT Ltd, HCL Tech and Moser Baer were among the major gainers.

Oil & Gas stocks tumbled as petrol prices were cut by Rs2 per lite and diesel by Rs1per litre. BPCL, HPCL and IOC were among the major losers.

Pharma stocks are mixed bag. Dr Reddy’s Lab surged 2.2% to Rs750, after the company entered in an accord with Torrent Pharma for selling drug in Russia, Cipla gained 2.2% to Rs254. however Ranbaxy slipped 2.8% to Rs369 and Sun Pharma was down 2.7% to Rs1015.Firmness may prevail

Strong Q2 GDP growth data, firm global markets and short covering in derivatives segment due to expiry of November derivatives contracts pushed Sensex up 80 points on Thursday (30 November). The market sentiment remains bullish due to strong FII-inflow and an upward revision in earnings growth of corporates by brokerages, on the back of strong Q2 results. The market would today eye monthly auto sales.

As per provisional data, FIIs were net buyers to the tune of Rs 88 crore on Thursday. Though FIIs were net sellers for the second day in a row on Wednesday (29 November), their outflow on that day of Rs 63 crore was much lower than Tuesday (28 November)’s Rs 335.30 crore.

Cumulative inflow of FIIs for November 2006 totaled Rs 9380.10 crore (till 29 November). FII inflow in November included their subscription to IPOs of Parsvnath Developers, Lanco Infratech and Info Edge India. There are expectations that FIIs may step up buying this month as allocations will be made for New Year calendar 2007.

But profit taking may cap further upside from the current level with the Sensex having risen sharply in the past few weeks. From 12,623.28 on 23 October, the BSE Sensex is up 8.5% in a little over a month.

Asian stock markets were mixed on Friday, with Japanese stocks rising and South Korean shares touching a six-month high, while Australia and Hong Kong dropped back from recent life highs.

US stocks ended little changed on Thursday as a report showing slowing Midwestern business activity offset gains in energy stocks on the back of rising oil prices. The Dow Jones industrial average fell 4.80 points, or 0.04 percent, to end at 12,221.93. The Standard & Poor's 500 Index rose 1.15 points, or 0.08 percent, to finish at 1,400.63. The Nasdaq Composite Index inched down just 0.46 of a point, or 0.02 percent, to close at 2,431.77.

Oil slipped more than half a percent, as profit-taking took the steam out of a four-session rally driven by a fall in US winter fuel stocks that had pushed prices to a two-month high above $63 a barrel. NYMEX crude for January delivery fell 34 cents to $62.79 a barrel, partially reversing a 67 cent rally on Thursday, when prices pushed up to their highest since Sept. 28.

November Reports

If you are looking for November posts - Go here

Do take a look at the Most Popular Pages for November

L.T.Overseas Ltd. Subscription Details

QIB - 8.39 times

NII/HNI - 4.29 times

Retail - 7.6 times

Overall - 7.18 times

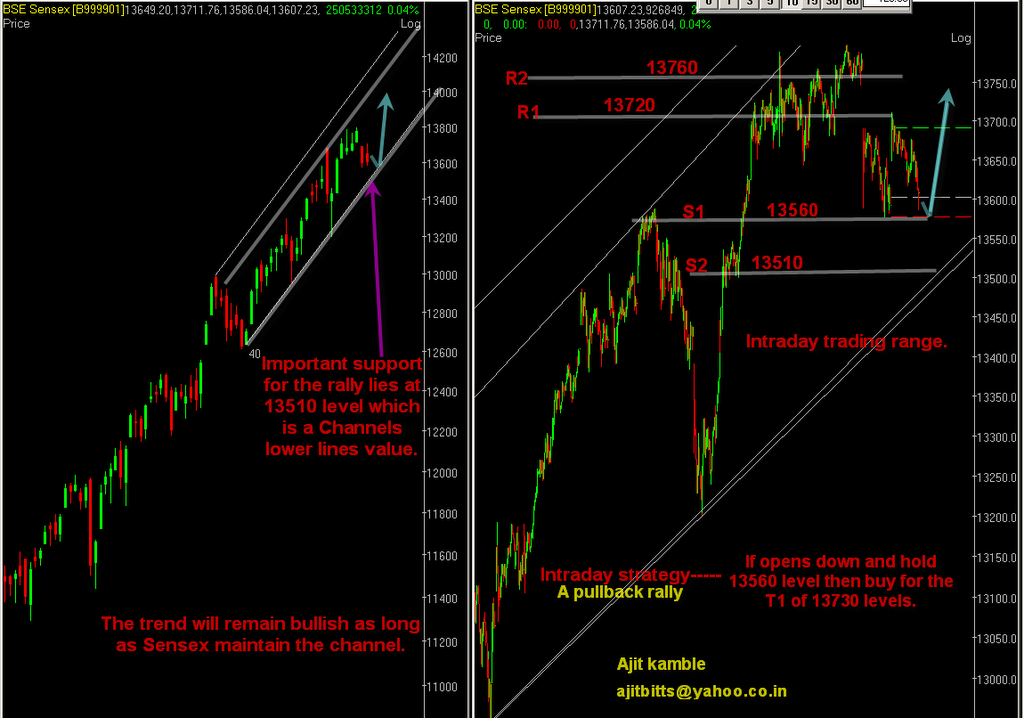

Technical Comment - Nov 30

(Click on the image to view Full Size)

It was a choppy session as Sensex opened with upside gap and attempted to fill the gap which it created on Tuesday but failed. In second half it slipped towards days low by violating the importance of 13650 levels which is a opening gap.

Sensex has formed a Bearish candle with higher upper shadow which indicates weakness in the trend i.e. the down trend witnessed a day earlier would remain intact. As of now Sensex is trading in a channel and still maintained the importance of channel. As per this channel important support lies at 13480 level which is a channels lower lines value. As long as Sensex maintain this level the bias seems to be positive and 14000 levels could be witness. Failure of this could lead to 13180 levels.

Subscribe to:

Posts (Atom)